The world is not experiencing a trade war. It is experiencing a fundamental restructuring of the global economic order — one Africa did not choose. For Nigeria and West Africa, the question is whether policymakers will act before the window closes.

01 — The Global Trade War: What Is Actually Happening

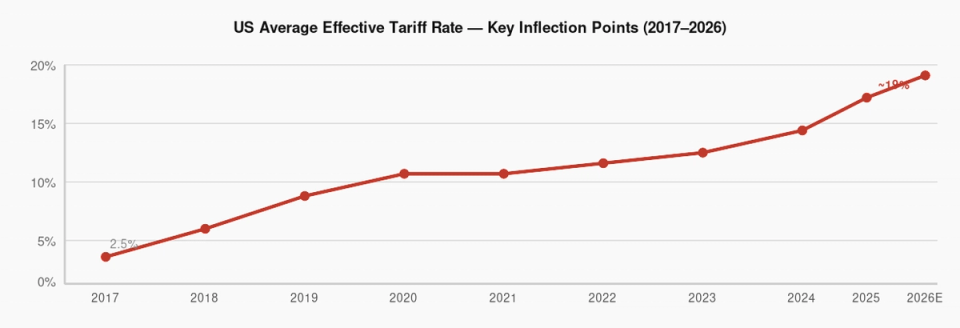

In January 2025, a returning US administration launched what would become the most sweeping unilateral restructuring of global trade architecture since the Bretton Woods era. Within four months, average US tariff rates climbed from 2.5% to approximately 22% — the highest since the early 20th century. The 145% tariff applied to Chinese goods reduced US imports from China by roughly half by June 2025, contracting bilateral trade flows to depths not seen since the 2009 financial crisis.

Exhibit 01 — US Average Effective Tariff Rate — Key Inflection Points (2017–2026)

Source: US International Trade Commission; Tax Foundation Tariff Tracker (2026); PIIE. Average effective tariff rate across all US imports. China-specific tariff peaked at 145% in April 2025.

China's response was not merely retaliatory — it was strategic. Beijing activated export controls on rare earth elements, accelerated yuan internationalisation through bilateral currency swap agreements, and aggressively expanded preferential trade access across the Global South. By June 2025, China had announced tariff-free access for 53 African nations, effective May 2026 — a direct counter-move to Washington's AGOA reconfiguration.

A US Supreme Court ruling in February 2026 struck down portions of the tariff programme. The administration responded with a sweeping 10% tariff on nearly all countries under Section 122 — applied to an estimated $1.2 trillion (34%) of annual US imports. The Tax Foundation characterised this as the largest US tax increase as a percentage of GDP since 1993, representing an average additional cost of $1,500 per US household in 2026.

The structure of global trade, stable for three decades, is being rewired in real time. The IMF estimates global trade flows have contracted between 5.5% and 8.5% relative to pre-shock baselines.

02 — The Visible Damage: What We Already Know

The headline consequences of the trade war are already measurable, and they are already falling disproportionately on the Global South. For Africa, four immediate channels of impact are in motion.

AGOA: Partial Extension, Fragmented Architecture

The African Growth and Opportunity Act lapsed on September 30, 2025. Congress extended it to December 31, 2026, but the extension is short-term, uncertain, and narrower in scope than the original. AGOA exports dropped 32% in the year ending November 2025 compared to 2024, according to the Trade Law Centre. Seven African nations now face a 15% US tariff on previously exempt goods. The strategic signal from Washington to African exporters is one of ambiguity — which, for investment planning purposes, functions identically to hostility.

Commodity Price Deterioration

Global commodity prices are projected to fall 12% through 2026, approaching a six-year low. Demand compression in a slowing China — the world's largest commodities buyer — and trade-war-induced industrial deceleration in the US have combined to suppress prices for oil, copper, iron ore, and most agricultural inputs. For SSA governments that derive 60–90% of export earnings from primary commodities, this is not a cyclical dip. It is a structural revenue reduction.

FDI Contraction

Sub-Saharan Africa could lose an estimated $10 billion annually in FDI and official development assistance — approximately 0.5% of GDP — as capital reprices risk in the current rate environment and redirects toward developed market assets offering historically attractive risk-adjusted returns.

03 — The Unseen Tremors: What Markets Are Not Pricing In

The consequences that attract headline coverage — tariff rates, GDP forecasts, AGOA expiry — are, paradoxically, the least consequential. They are already priced. The more structurally important disruptions are the ones that have not yet fully manifested, and which are not yet informing African policy postures with sufficient urgency.

Dollar Weaponisation and the African Debt Trap

The Federal Reserve's sustained elevated rate posture has maintained the dollar at historically strong levels. For African governments servicing dollar-denominated external debt, this creates a compounding fiscal trap: commodity revenues decline while debt service obligations rise in local currency terms as the dollar strengthens. Kenya has already restructured dollar-denominated debt into Chinese yuan. Ethiopia is in similar negotiations. These moves represent the early stages of a structural shift in African public finance architecture that will accelerate as more governments reach debt stress thresholds through 2026–2027.

Rare Earth Reordering: Africa's Unleveraged Strategic Asset

China's export controls on rare earth elements — gallium, germanium, and critical battery precursor materials — have exposed a structural vulnerability in the global technology supply chain. Seventeen of the world's 30 most critical minerals are present in significant deposits across Sub-Saharan Africa. As both Washington and Beijing race to secure alternative supply chain access, African mineral-holding governments should be commanding a premium in these negotiations. The evidence suggests they are not. Concession agreements being concluded in 2025–2026 reflect the negotiating weakness of individual African governments, not the strategic value of the assets they control.

The China+1 Trade Diversion: Asia's Boom, Africa's Missed Moment

When US-China decoupling intensified post-April 2025, Southeast Asian economies — Vietnam, Malaysia, Thailand, Indonesia — became the primary beneficiaries of trade diversion. Africa has not captured equivalent manufacturing flows, despite being structurally positioned to benefit. Nigeria's Lekki Free Trade Zone, the Ogun-Guangdong Free Trade Zone, and Ethiopia's Hawassa Industrial Park were designed for precisely this kind of moment. The execution gap remains Africa's policy failure. The window remains open — but Southeast Asian location advantages are being locked in through long-term supply agreements that are compressing the timeline for African entry.

The Invisible Inflation Tax: Chinese Overcapacity and African Markets

As US tariffs reduce China's access to American consumers, Chinese export overcapacity seeks alternative markets. Africa — with relatively open borders, limited anti-dumping frameworks, and large import-dependent consumer markets — becomes a natural pressure release valve. The resulting flood of competitively priced Chinese finished goods simultaneously provides short-term consumer price relief and systematically suppresses African manufacturing competitiveness. Nigeria recorded its largest bilateral trade deficit with China in recorded history in 2025 — against an overall national trade surplus of N17.78 trillion.

The Food-Fertiliser-Freight Nexus: The Slow Emergency

Three compounding supply chain disruptions — Ukraine-Russia war disruption to fertiliser supply, Red Sea shipping route instability from Houthi attacks, and the trade war's repricing of freight logistics — have created a structural cost floor for African agricultural production that is still transmitting through the supply chain. Food consumer price inflation exceeded 5% in 45% of low-income countries as of November 2025. These disruptions typically reach African retail markets with a 9–18 month lag. The full consumer impact of 2025 supply chain pressures has not yet been felt.

04 — Africa at the Epicentre: Caught Between Giants

Africa entered this global reconfiguration in a structurally precarious position — but not without agency. The continent's trade architecture, built on raw material exports and manufactured good imports, maximises exposure to commodity price volatility while minimising participation in the value-added activities where economic surplus is concentrated. The AfCFTA was designed precisely to address this structural weakness. Implementation has lagged ambition.

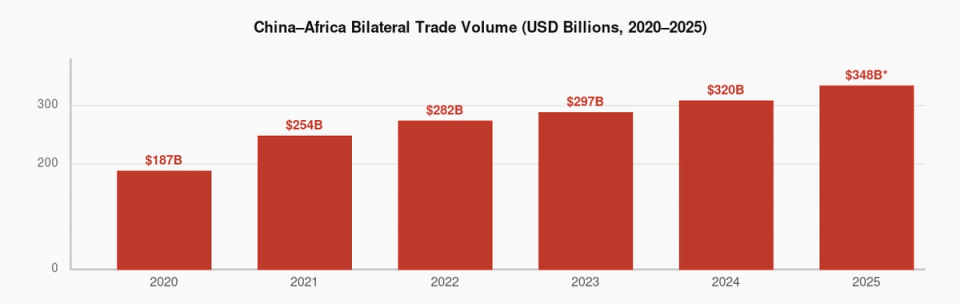

China-Africa bilateral trade reached a historic $348 billion in 2025 — a 17.7% year-on-year increase. But the composition tells the structural story: Africa exports primary commodities; China exports finished electronics, vehicles, textiles, building materials, and industrial machinery. The IMF estimates a full structural split between the major economic powers could cost Africa 4% in lost economic growth — more than any other region. For a continent where 600 million people still lack reliable electricity and 300 million face food insecurity, 4% of GDP is not a statistical variance. It is generational setback.

Exhibit 02 — China–Africa Bilateral Trade Volume (USD Billions, 2020–2025)

Source: China Ministry of Commerce; Al Jazeera (Jan 2026). *2025 figure represents annual total. +17.7% year-on-year growth.

China's tariff-free access pledge for 53 African nations — announced June 2025 — is the most substantive economic gesture made to Africa since AGOA's inception in 2000. But the architecture of the offer must be read carefully. China's duty-free framework is primarily designed to facilitate Chinese investor access to African raw materials and to build export market share for Chinese finished goods — not to catalyse African value-added manufacturing or indigenous industrial development.

05 — Sub-Saharan Africa: Structural Vulnerabilities Laid Bare

The Debt Compression Spiral

Combined debt service obligations across multiple SSA economies now consume between 25% and 50% of government revenues — fiscal space that would otherwise fund health systems, education, and physical infrastructure. Ghana, Zambia, and Ethiopia are the visible restructuring cases. The pipeline of governments approaching fiscal stress thresholds is considerably longer than the cases currently attracting multilateral attention.

A critical structural concern: the Common Framework for Debt Treatment — designed to bring China into coordinated multilateral restructuring processes — has moved with insufficient speed. China's approach to debt restructuring has consistently prioritised bilateral negotiation over multilateral frameworks, resulting in terms that are highly variable, non-transparent, and often more favourable to Chinese creditor interests than comparable Paris Club arrangements.

The Technology Infrastructure Bifurcation

The US-China decoupling is simultaneously a technology architecture story — involving semiconductors, AI infrastructure, cloud platforms, telecommunications networks, and digital payment systems. African governments are making infrastructure decisions today — 5G network vendor selection, cloud service provider agreements, digital payment rail architecture — that will embed their economies in either the US-aligned or Chinese technology ecosystem for 15–20 years. These decisions are being made without adequate geopolitical intelligence analysis of their long-term strategic consequences.

06 — West Africa: Fault Lines Under Pressure

The Sahel Security Cordon and Its Economic Costs

The political collapse of Burkina Faso, Mali, and Niger — their departure from ECOWAS and the establishment of the Alliance des États du Sahel — has created a security and economic fault line running across West Africa's northern tier. These landlocked economies depend on coastal ports in Abidjan, Dakar, Lomé, Tema, and Lagos for access to global markets. The disruption of this transit corridor through political tension, trade sanctions, and physical insecurity has added a structural cost premium to West African trade logistics. Freight costs within West Africa already absorb up to 40% of the end price of traded goods.

The CFA Franc Question: Stability With a Cost

The CFA franc — pegged to the euro and backstopped by the French Treasury — provides monetary stability for the eight WAEMU member states at the cost of autonomous monetary policy. As the euro weakened against the dollar through 2025–2026, CFA-zone commodity exporters selling goods priced in dollars experienced deteriorating terms of trade. The political momentum to restructure or exit the CFA arrangement has accelerated in Senegal, Côte d'Ivoire, and Togo — without yet reaching policy resolution.

The Cocoa Anomaly and Its Limits

Côte d'Ivoire and Ghana — the world's first and second largest cocoa producers — have benefited from elevated cocoa prices, one of the few commodity categories bucking the global deflationary trend. This divergence between cocoa-rich coastal economies and oil-dependent or commodity-poor inland economies is creating internal tensions within the ECOWAS integration project at the precise moment when regional solidarity is most strategically important.

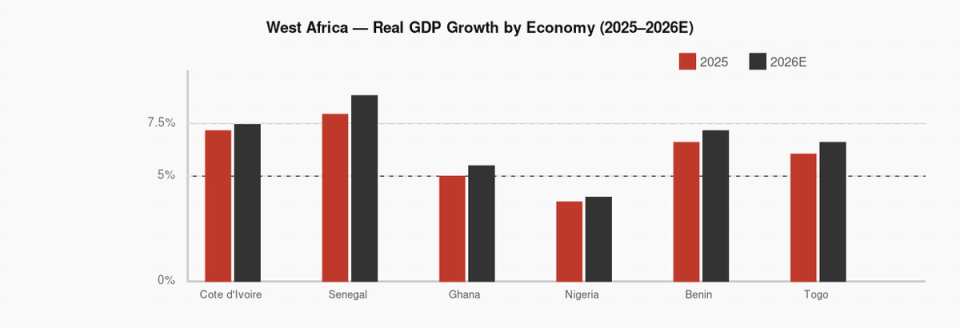

Exhibit 03 — West Africa — Real GDP Growth by Economy (2025–2026E)

Source: Deloitte Africa Economic Outlook (Nov 2025); UNECA (2026); World Bank projections. West Africa growth remains solid but conceals divergence between oil-dependent and diversified economies.

07 — Nigeria: A Pivotal Moment Disguised as a Crisis

Nigeria enters 2026 with a paradox that its policymakers have not yet fully resolved: its macroeconomic architecture has achieved a degree of stabilisation at the same moment that its structural exposure to the global trade war has intensified. The stabilisation is real. The structural exposure is also real. The mistake is to read the former as resolution of the latter.

The Fiscal Arithmetic

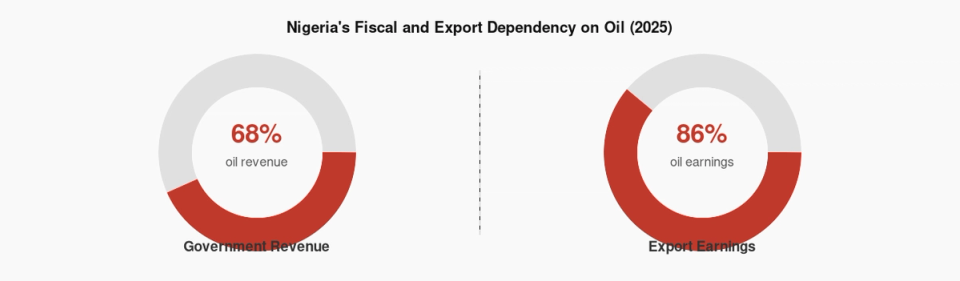

Oil still accounts for 65% of government revenue and 86% of exports. With Brent crude trading below $61 per barrel in early 2026 — against the 2026 budget benchmark of $64.85/barrel — each dollar of sustained price decline translates to approximately $500 million in annual revenue shortfall. Nigeria has additionally missed its OPEC production quota of 1.5 million barrels per day for six consecutive months, producing between 1.31 and 1.46 mbpd due to oil theft, pipeline vandalism, and chronic underinvestment in Niger Delta extraction infrastructure. Crude oil export earnings fell from $36.85 billion in 2024 to $31.54 billion in 2025 — a $5.31 billion year-on-year decline.

Exhibit 04 — Nigeria's Fiscal and Export Dependency on Oil (2025)

Source: CBN Macroeconomic Outlook 2025; World Bank Nigeria Economic Update (Oct 2025). Oil remains the overwhelming source of government revenue and export earnings despite a decade of diversification rhetoric.

The Naira: Stabilised but Not Transformed

The naira has achieved a degree of stability following the 2023–2024 reform and devaluation sequence. Foreign reserves have rebuilt to $42 billion. Inflation has fallen to 15.06% — the lowest since November 2020 — after eleven consecutive months of decline. These are genuine macroeconomic achievements. But stabilisation of a structurally unreformed economy is not transformation. Nigeria has created conditions for growth without yet constructing the industrial architecture through which that growth can be sustained and diversified.

The China Trade Deficit: A Structural Warning in Plain Numbers

Nigeria recorded its largest bilateral trade deficit with China in recorded history in 2025 — against an overall national trade surplus of N17.78 trillion. Bilateral China-Nigeria trade exceeded $22.3 billion in the first ten months of 2025, a 30% year-on-year increase. The composition tells the structural story: Nigeria exports crude oil and unprocessed agricultural commodities; China exports finished electronics, vehicles, textiles, building materials, pharmaceuticals, and industrial machinery. This is not a partnership of economic equals. It is a replication of the colonial extraction-and-import trade architecture under a different flag.

The Dangote Variable: Africa's Most Consequential Industrial Bet

The Dangote Petroleum Refinery — now scaling operations at Lekki — represents the most structurally significant intervention in Nigeria's energy economics since the construction of the Escravos terminal in 1989. At its 650,000 barrel-per-day design capacity, it eliminates Nigeria's defining structural paradox: being Africa's largest oil producer while importing 80–90% of its refined petroleum products. The elimination of PMS import dependency — currently consuming an estimated $10–15 billion annually in foreign exchange — will progressively free capital that can be redirected toward domestic investment.

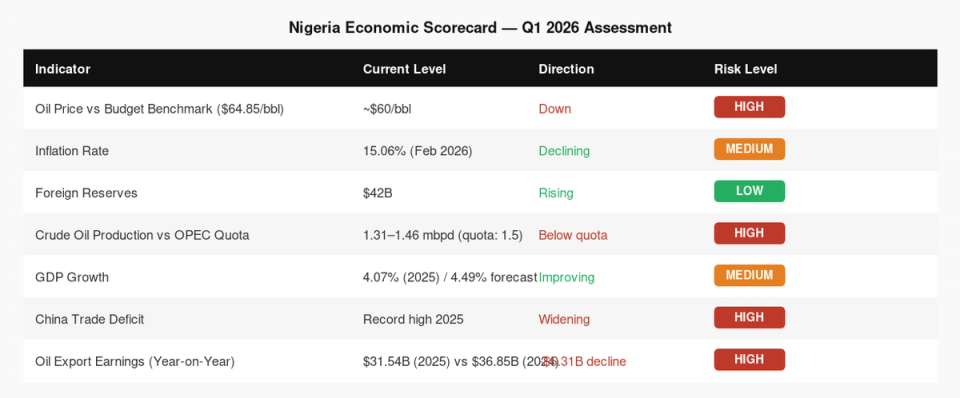

Exhibit 05 — Nigeria Economic Scorecard — Q1 2026 Assessment

Source: CBN; NBS; ICIRNIGERIA; OPEC; World Bank. Scorecard reflects Carthena Advisory assessment as of March 2026.

The Manufacturing Window: Open but Not Permanent

The global trade war has created an unexpected structural tailwind for Nigerian manufacturing. As Southeast Asian manufacturing wages rise and US-China supply chain decoupling incentivises procurement diversification, Nigeria's combination of a 220-million-consumer domestic market, improving port infrastructure through the Lekki Deep Sea Port, existing industrial zone frameworks, and a more competitive naira positions it as a credible alternative manufacturing destination. The binding constraints are well-documented: power supply reliability, regulatory process predictability, customs administration efficiency. These are not structural impossibilities. They are execution failures. Nigeria has approximately a 24–36 month window to position itself credibly before the reallocation is complete.

08 — The Lagging Effects: What Is Still Coming

Multilateral Trade Architecture Collapse

The WTO's dispute resolution mechanism is effectively non-functional. The rules-based trading order constructed between 1995 and 2015 is being replaced by a system of bilateral and plurilateral agreements negotiated under conditions of significant power asymmetry. Africa, without a unified and technically capable trade negotiating bloc, is structurally positioned as a rule-taker in this new environment. AfCFTA implementation is not merely an economic integration project — it is a geopolitical prerequisite for Africa's ability to exercise meaningful sovereignty in the emerging trade order.

The Debt Restructuring Wave

Multiple SSA governments are in various stages of debt distress. The pace of restructuring will accelerate through 2026–2028. The terms of these restructurings — the degree to which they preserve or erode fiscal sovereignty and the precedents established for future creditor-debtor relationships — will shape African development financing for a decade.

The Climate Finance Squeeze

The diplomatic bandwidth and domestic political capital of major economies — the primary funders of African climate adaptation — is being consumed by trade war management. The $100 billion annual climate finance commitment remains unmet. G7 development finance institutions face budget pressure as donor governments redirect resources toward domestic economic stabilisation. The consequences of underfunded climate adaptation will arrive with climatic precision regardless of political timelines.

The Fertiliser-Food Lag

Fertiliser prices, global freight rates, and food commodity prices are still transmitting through African supply chains with an estimated 9–18 month lag from their 2025 disruption origin. The retail food price impacts of 2025's compound supply chain stress will fully manifest across SSA markets through Q3 2026 and beyond. Social stability implications in food-import-dependent urban populations — Lagos, Accra, Dakar, Nairobi — warrant proactive food security policy attention.

09 — Carthena Advisory: Strategic Imperatives for Nigeria and West Africa

The current global disruption is not primarily a crisis. It is a structural transition — one that will resolve not by restoring the pre-2025 trade order, but through the emergence of a new one. The question for Nigeria and West Africa is not how to survive the transition. It is how to shape their position within the architecture that follows.

01 — Negotiate from Strategic Strength, Not Fiscal Desperation

Nigeria's minerals portfolio — lithium, cobalt precursors, tantalum, and strategic agricultural commodities — carries elevated strategic value in a world restructuring supply chains away from Chinese dependency. These assets should be deployed as leverage in trade negotiations with both Washington and Beijing, not offered at concessional terms to the first party that arrives with a cheque. The government requires a dedicated Minerals Geopolitical Strategy with cross-ministerial authority to ensure that concession agreements concluded in 2026–2028 reflect strategic value, not negotiating weakness.

02 — Convert AfCFTA from Declaration to Infrastructure

Intra-African trade at 17% of total trade is both an indictment of regional integration and an enormous strategic opportunity. Nigeria must convert rhetorical AfCFTA support into active implementation investment: funding the Pan-African Payment and Settlement System (PAPSS) to full operational scale, harmonising customs procedures at the Seme border, and committing capital to the transport corridors that make regional trade logistically competitive with import alternatives. The geopolitical case for intra-African trade is now stronger than it has ever been.

03 — Treat the Dangote Refinery as a National Economic Transformation Moment

The elimination of petroleum product import dependency frees an estimated $10–15 billion annually in foreign exchange. This capital — if channelled through deliberate fiscal and investment policy rather than diffusing into the informal economy — represents the largest potential source of incremental domestic investment Nigeria has ever had access to. Government must develop an explicit framework for how refined petroleum savings will be directed toward capital formation, debt service reduction, and manufacturing sector investment.

04 — Build the Regulatory Infrastructure for FDI Before the Window Closes

Nigeria has the market, the geography, and improving physical infrastructure to capture trade diversion manufacturing flows. What it lacks is regulatory predictability and execution certainty. The government must demonstrate — through consistent CBN FX policy, transparent dispute resolution, and accelerated one-stop-shop processing — that investment commitments made in Nigeria will be honoured. The 24–36 month window before Southeast Asian manufacturing advantage is locked in through multi-year supply agreements is not generous. The regulatory reform agenda requires wartime execution pace.

05 — Establish a Geopolitical Trade Intelligence Function at the Centre of Government

The speed and complexity of the current global trade reconfiguration has exposed a critical capacity gap in Nigerian policy institutions: the absence of real-time geopolitical trade intelligence. The Ministry of Finance, CBN, Ministry of Trade and Investment, and the Nigerian Export Promotion Council require a coordinated analytical function — staffed with trade economists, geopolitical analysts, and supply chain specialists — capable of identifying emerging trade diversion opportunities and providing decision-relevant assessments of geopolitical developments before they become policy crises. Africa's most consequential negotiating failures are intelligence failures first.

A Final Word: The Moment and Its Demand

The architecture of the global economic order is being redrawn by forces that African governments did not initiate and cannot unilaterally arrest. But the history of economic development offers a consistent lesson: structural disruption consistently creates the conditions for industrial emergence for those governments with the analytical clarity to identify the opportunity and the institutional capacity to execute against it. Korea, Taiwan, and Singapore emerged from post-war disruption. Vietnam, Malaysia, and Bangladesh emerged from the first US-China trade war of 2018–2019.

The question of whether Nigeria — and West Africa more broadly — will emerge stronger from the current restructuring is not a question about global forces. It is a question about policy quality, institutional capacity, and the willingness of African governments to negotiate with the strategic confidence that their assets and their markets warrant.

The gap between what Africa's assets are worth in this new geopolitical moment and the terms on which those assets are currently being traded is not a market problem. It is an intelligence problem — and intelligence problems are solvable. — Carthena Advisory, March 2026